The coming year promises to bring a host of new opportunities and challenges in the world of pensions. So many consultations, legislative changes and updated pieces of guidance, make it difficult to keep up. This post makes it easier to follow next year’s range of developments by grouping them into seven themes.

We’ve also brought together a comprehensive list of all of the key dates for pensions in 2022. Click here to go straight to our key date planner.

1. Extending TPR’s powers and A Single Code to guide them all

1 October 2021 saw a material extension in The Pension Regulator’s (TPR) powers when key provisions of The Pension Schemes Act 2021 came into force (click here for our Insight ‘Pensions law is changing on 1 October 2021 – Are you ready? (29 September 2021)’).

In the coming year, TPR will:

- gain additional powers (with an extension to its notifiable events regime to cover certain corporate transactions expected to come into force on 6 April 2022);

- complete its criminal sanctions and enforcement policies by issuing the final versions of policies covering:

- what TPR will do if there are overlapping enforcement powers available to it;

- the levying of ‘high fines’ (i.e. financial penalties of up to £1 million); and

- the use of its broadened information gathering powers; and

- lay the final version of its single code of practice before Parliament (this is expected to happen in Spring 2022 with the code going into force in Summer 2022). The single code of practice will bring together 10 out of 15 of TPR’s existing codes of practice (with the remaining five expected to be incorporated into the single code of practice in due course).

Of these, the extension of the notifiable events regime will be of greatest concern to scheme sponsors (click here for our Insight ‘Will your corporate activity be captured by new pensions notification requirements (23 September 2021)’). Trustees are likely to be watching out for what is in the final version of TPR’s single code of practice.

2. A new approach to funding defined benefit schemes takes final shape

In 2021, the DWP and TPR were expected to publish final regulations and guidance respectively on a new approach to funding defined benefit schemes. The Pension Schemes Act 2021 sets out the legal framework permitting a new scheme funding regime. The detail for the new regime will, however, be set out in:

- secondary legislation; and

- a revised code of practice on defined benefit scheme funding.

Both of these have now slipped into 2022. In addition, TPR published a blog post stating that it will need more time to develop its revised code of practice on DB funding. As a result, the second consultation on its revised code of practice will be published in late summer 2022 rather than in spring 2022.

This delay could have an impact on the timing of when the funding regime goes into force. It remains possible that the new regime will come into force at the end of 2022. It does, however, seem more likely that it will be early 2023 before the new funding regime applies. Under the new regime, trustees will need to:

- determine a scheme-specific funding and investment strategy (also referred to as the ‘long term objective’);

- have a written statement setting out their strategy; and

- submit a version of the statement of strategy signed by the chair of trustees to TPR.

Click here for our more detailed blog post on defined benefit funding in 2022.

3. Environmental, Social and Governance policies extend their reach

On and from 1 October 2022, schemes with assets of more than £1 billion will be subject to the climate change governance and reporting regime. This will increase its reach from the current 100 schemes to approximately 340 schemes. The investments held by this bigger group will be more than double the current amount (increasing from £700 billion to £1.45 trillion). Climate risk monitoring and reporting will enter the mainstream in pensions.

In addition, these schemes will have an additional reporting metric. On and from 1 October 2022, schemes will have to measure and report on the extent to which their investments align with the Paris Agreement (i.e. the intention to limit the global average temperature increase to within 1.5°C above pre-industrial levels). Amended guidance sets out the detail of how trustees will need to comply with this additional requirement.

The DWP is also consulting on proposed guidance covering trustee stewardship and how stewardship policies are communicated via Implementation Statements and SIPs. The proposed guidance will come into force in 2022.

Click here for our more detailed blog post on ESG developments and pensions in 2022.

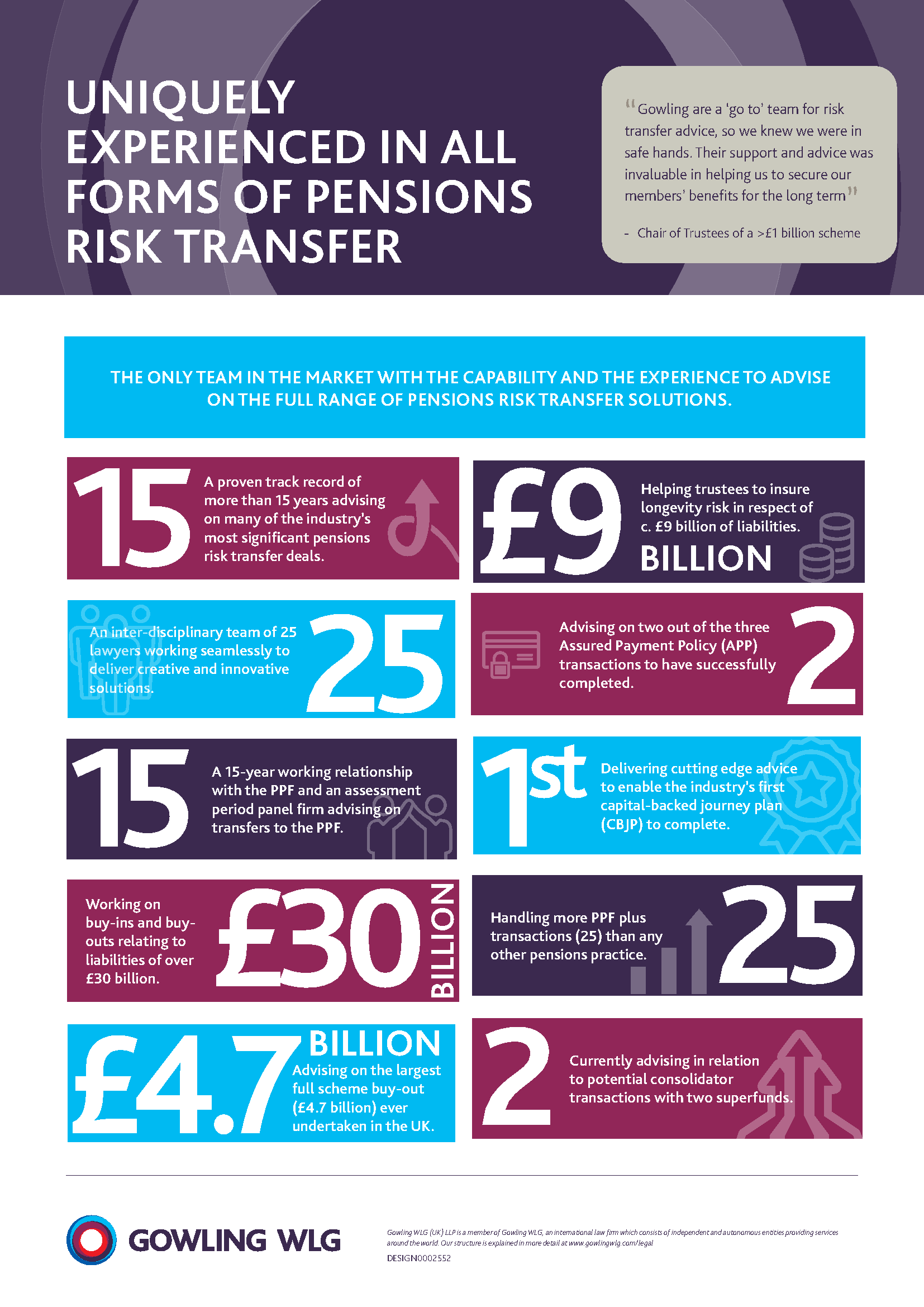

4. A record breaking year for risk transfer

In 2020, a record-breaking £55.8 billion of pension scheme liabilities were transferred. In 2022, this figure is likely to be exceeded. One major consultancy has predicted that up to £60 billion worth of pension scheme liabilities will be transferred in 2022.

The prediction is based on pent-up levels of demand to transact, improvements in DB scheme funding levels, moves to de-risk investments, improvements in data quality and clear plans to address GMP equalisation. And it isn’t only the value of transactions that is increasing. Next year is also likely to see:

- a number of extremely large trades; and

- the more widespread use of a range of risk transfer solutions (with longevity swaps being highlighted as becoming increasingly popular).

These predictions align with the experience and expectations of our industry-leading Pensions Risk Transfer team. In the past few years, they have been involved in a number of firsts on risk transfer (click here for an overview of the range of risk transfer activity this encompasses).

In addition to traditional risk-transfer solutions, 2022 will see the development and perhaps even the launch of the UK’s first collective defined contribution (CDC) scheme. Royal Mail has just completed a consultation with its unions and staff. Subject to:

- the outcome of that consultation;

- regulations being finalised and made (with the government targeting 1 August 2022 as the date that the legislation will come into force); and

- TPR authorisation

The Royal Mail Collective Pension Plan will be launched next year.

It is likely that 2022 will also be the year that we find out if the Royal Mail’s scheme will be a one-off or a trail-blazer for an exciting new mode of pension provision.

Finally, 2022 is likely to be the year that we see the first superfund transaction. At the end of November, TPR issued its first authorisation for a superfund. In 2022, we could also see TPR authorise a second superfund. It could be that developments in this space open the door to more providers to offer superfund propositions.

5. Getting ready for a revolution in member communications

In 2022, there will be two key developments that will change member communications for certain schemes. The first is that schemes will be required to provide a ‘stronger nudge’ to pensions guidance. This is planned to come into force on and from:

- 6 April 2022 for schemes regulated by TPR; and

- 1 June 2022 for schemes regulated by the FCA.

The second is the roll out of simpler annual benefit statements from 1 October 2022. These will initially apply to defined contribution schemes that are used for automatic enrolment. It is possible that they will gain more widespread use if they are well received by members.

Perhaps the biggest change won’t happen in 2022 but in 2023 with the launch of pensions dashboards. However, a huge amount of work will be carried out in 2022 to get ready for this launch. As part of this, we can expect:

- the DWP to consult on regulations;

- the Pensions Dashboards Programme to issue further calls for evidence, guidance and standards; and

- the Pensions Dashboards Programme to enter the alpha phase of testing and roll out.

6. Changing charge caps in DC-based automatic enrolment schemes

In 2021, the DWP issued two consultations on changes to the default fund charge cap for DC-based automatic enrolment pension schemes in certain circumstances. The consultations:

- covered the introduction of a £100 de minimis threshold that will apply to flat fees paid in DC-based automatic enrolment schemes. From 1 April 2022, DC-based automatic enrolment schemes will no longer be able to charge a flat fee to all pension savers; and

- set out proposals to allow trustees of DC-based automatic enrolment schemes to exclude performance-based fees from the regulatory charge cap. This open consultation is part of Budget measures designed to facilitate more investment in illiquid asset classes. The government is proposing that trustees will be allowed to exclude ‘well-designed’ performance fees from the 0.75% charge cap. The consultation closes on 18 January 2022 and the government aims to issue a response in early 2022.

7. Take two for public service pension reform

The Public Service Pensions Act 2013 provided for changes to be made to the benefit structure of public service pension schemes. The result was the introduction of new versions of public service pension schemes. A number of trades unions opposed the reforms and backed legal action against the government.

In two key cases (McCloud and Sargeant), the Court of Appeal held that transitional protections were discriminatory against younger members of the judicial and firefighters’ pension schemes respectively. The government acknowledged that these judgments would impact other public service schemes. A consultation in 2020 was followed by a government response in 2021. The result is that 2022 will see the introduction of reformed public service pension schemes. From 1 April 2022, all those who continue in service will do so as members of the reformed schemes.

What else is on the cards for 2022?

Our seven key themes pack in a lot of developments which will keep the pensions industry busy throughout 2022. In addition, there are a few miscellaneous developments which are worth noting.

GMP Conversion Bill

Private Members’ Bills are introduced by individual MPs rather than the government. They are usually given short shrift by the government and rarely make the statute books. Next year could see an exception to that general rule.

The Pension Schemes (Conversion of Guaranteed Minimum Pensions) Bill (the Bill) is currently at committee stage in the House of Commons. Unusually for a Private Members’ Bill, it seems to be getting support from the government (for example, the DWP drafted the Explanatory Note). If the Bill becomes law, it will simplify the GMP conversion process and should, therefore, be welcomed by many in the pensions industry.

Normal Minimum Pension Age increase legislation

The Finance (No. 2) Bill 2021 / 22 contains provisions to increase the Normal Minimum Pension Age (NMPA) from 55 to 57. The change will take effect on 6 April 2028.

Although the increase to NMPA is not for a number of years, the Bill will become law in 2022. In addition, it will create a new preservation right (the detailed mechanics of which are not yet clear) that members may seek to take advantage of well in advance of 2028.

Bringing the CMA Order into pensions law

The Competition and Markets Authority (CMA) carried out an investigation into investment consultancy and fund management services to pension schemes. This resulted in an Order which came into force on 10 December 2019. Trustees have until 7 January 2022 to confirm to the CMA that they have complied with the requirements of the Order.

In addition, the government promised to bring the effect of the Order into pensions legislation. To this end, the DWP consulted on regulations. It is likely that these regulations will come into force in 2022.

Ian Chapman-Curry

{kind=link}

Ian is a London-based professional support lawyer (PSL) legal director. Ian is a member of our pensions and combined human resource solutions (CHRS) teams. He works with clients to solve their employment and pensions law issues. Ian maintains a particular focus on 'crossover' issues that benefit from his understanding of both areas of law.