The last few years have seen pension scheme liabilities transferred in record-breaking numbers. Reports on the bulk annuity market highlighted trades totalling around £43 billion in 2019. Even the more subdued, COVID-19 impacted 2020 saw £32 billion worth of liabilities transferred. Even in this challenging year, reports on the wider UK pensions risk transfer market declared record-breaking numbers. Risk totalling £55.8 billion was transferred, exceeding the previous non-pandemic year.

What has the market been like for risk transfer over the pandemic?

The total risk transfer market in 2021 is predicted by one consultancy to close at nearer to £45 billion, with the market reportedly dominated by comparatively smaller trades (without some of the mega-deals that had been seen in previous years). Nonetheless, market observers predict close to £30 billion of bulk annuity deals alone being completed this year.

This lower level is understandable given the existential threats being faced by some businesses. With additional constraints on management time, there has been less appetite for the limited remaining focus to deal with tomorrow’s problems like pension schemes.

Trustee boards have also been focussed on more immediate concerns, like how to run a multi-million pound pension scheme out of the family shed, where the mute button is located, and how to ensure a market downturn didn’t wipe-out any recent funding gains their scheme may have seen before the pandemic.

Nonetheless, the market remained strong in 2021.

With Trustee boards’ time taken up on other matters in the latter part of 2020, fewer were ready to approach the market in early 2021. However, as the year progressed and the weather warmed-up, so too did the market, with most predicting that 2021 would see bulk annuity trading levels similar to 2020, driven by some highly competitive pricing in the year. Schemes that already had their funding in place and had done their homework in preparation for going to market ensured that demand remained strong.

What are the prospects for risk transfer in 2022?

With Aon reporting that buying-out has moved ahead of self-sufficiency for the first time as the preferred solution in trustees’ long-term planning, the market is poised to go from strength-to-strength, with many predicting that records set in previous years will soon be smashed.

Mercer has predicted that trustees will transfer £60 billion of risk in 2022 including bulk annuities and the longevity swap market.

And it isn’t only the value of transactions that is increasing. Next year is likely to see a large number of extremely large trades and the more widespread use of a range of risk transfer solutions (with longevity swaps highlighted as becoming increasingly popular).

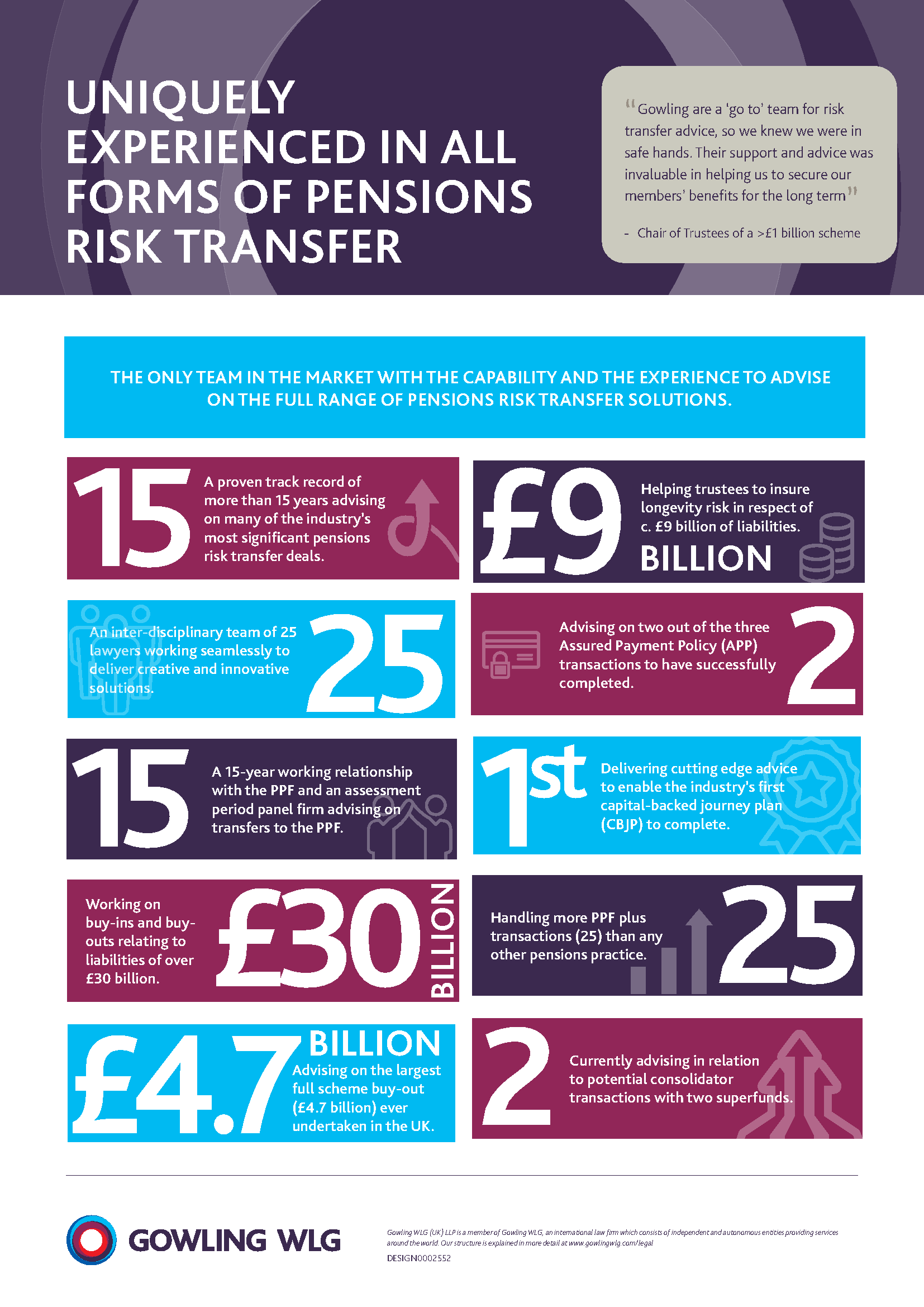

This aligns with the experience and expectations of our industry-leading Pensions Risk Transfer team. In the past few years, they have been involved in a number of firsts on risk transfer (click here for an overview of the range of risk transfer activity this encompasses).

{kind=link}

Insurers too are reportedly responding to this expected growth by developing their own teams to expand capacity in the market.

Capacity could still be an issue, with our team’s experience suggesting that schemes will need to be well-prepared to take advantage of arising opportunities, with some schemes likely to be squeezed out in favour of those deemed more ready to transact. We have seen the advantages that a well-prepared scheme has in going to market, as well as the problems that can arise for those whose due diligence has perhaps been lacking.

Data quality, funding, and clarity over the benefit structure are all key to effecting a smooth transaction, as are clarity and flexibility in trustees’ expectations as to when they wish to transact. Schemes that are looking to take advantage of opportunities in the short-term should ensure that they are not held back by any hidden gremlins. Early engagement of legal advisers can materially help smooth schemes’ path to de-risking.

Moving beyond the norm

2022 will see the development and perhaps even the launch of the UK’s first collective defined contribution (CDC) scheme. Royal Mail has just completed a consultation with its unions and staff. Subject to:

• the outcome of that consultation;

• regulations being finalised and made; and

• the Pension’s Regulator’s (TPR) authorisation

the Royal Mail Collective Pension Plan will be launched next year.

It is likely that 2022 will also be the year that we find out if the Royal Mail’s CDC scheme will be a one-off or a trailblazer for an exciting new mode of pension provision.

Finally, 2022 is likely to be the year that we see the first superfund transaction. At the end of November, TPR issued its first authorisation for the Clara superfund. In 2022, we may see TPR authorise a second superfund. It could be that this opens the door to more providers to offer superfund propositions.

About the author(s)

Ian is a London-based professional support lawyer (PSL) legal director. Ian is a member of our pensions and combined human resource solutions (CHRS) teams. He works with clients to solve their employment and pensions law issues. Ian maintains a particular focus on 'crossover' issues that benefit from his understanding of both areas of law.

Ian Chapman-Curry

Ian is a London-based professional support lawyer (PSL) legal director. Ian is a member of our pensions and combined human resource solutions (CHRS) teams. He works with clients to solve their employment and pensions law issues. Ian maintains a particular focus on 'crossover' issues that benefit from his understanding of both areas of law.